This sentence, from an article in the Financial Times of 20 April 2025, gives a good idea of what is happening in the trade war between the US and China: the latest controls on Chinese exports of rare earth minerals could bring automotive production to a standstill, with stocks of essential magnets set to run out within months if Beijing completely stifles exports.

The story is being played out again now, in June 2025 : ” Exports from China to the US -34% in May⏬

a key issue is related to rare earths, of which the Chinese have a near-monopoly in some cases and which are a key element in the production of e.g. certain car components

the industry fears that this on rare earths could be the third supply shock in the last 5 years after covid and the semiconductor crisis.

Below you will find an article by Milena Gabbanelli that makes you realise how far ahead of Westerners the Chinese were in 2021 on this topic.

This article talks mainly about metals.

Commodities, rising prices: braking the ecological and digital transition. The role of China

by Milena Gabanelli and Rita Querzè

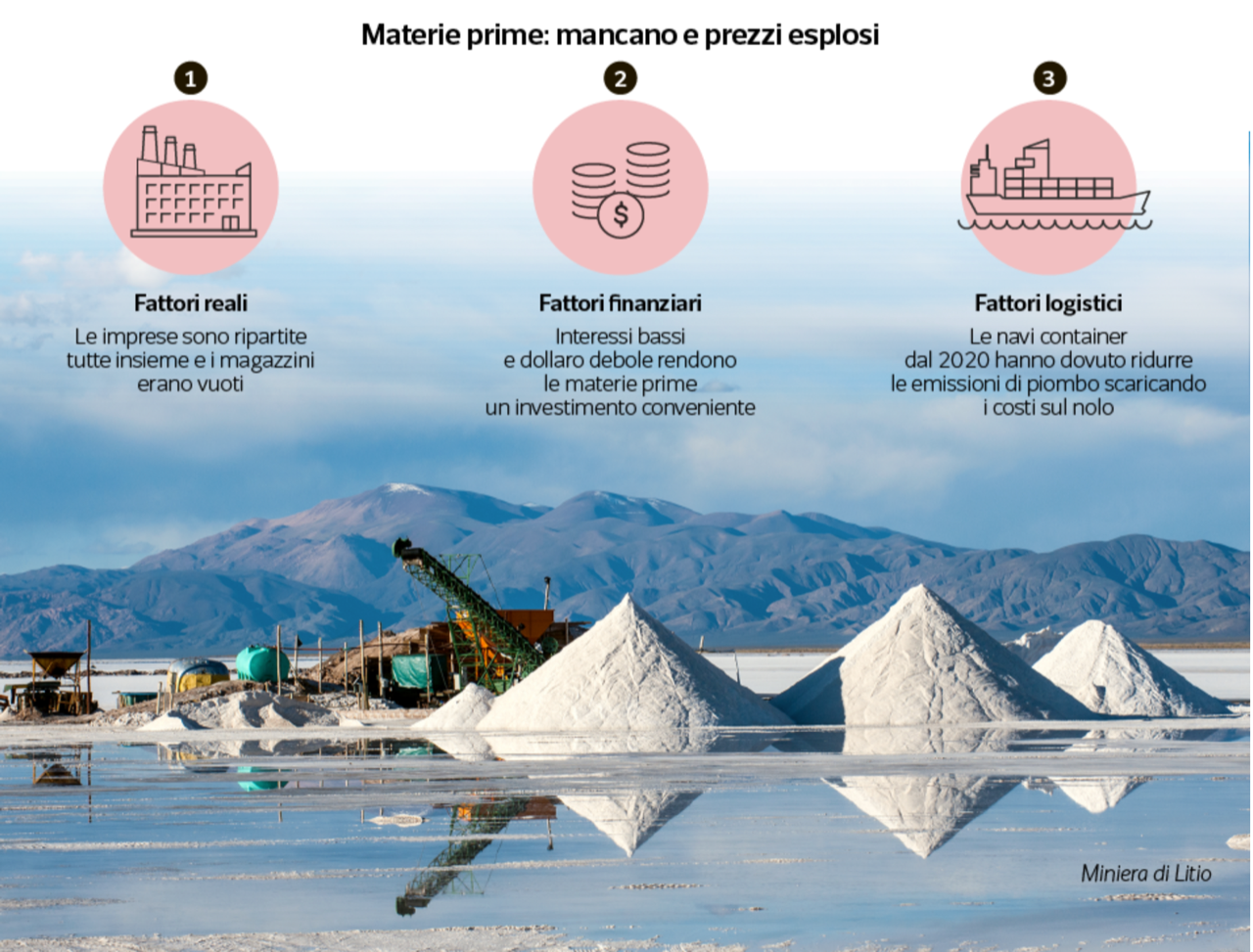

Household appliance, furniture, food, car factories are all grinding to a halt. Just when demand is picking up again. The issue is that almost all raw materials have become unavailable and very expensive. The British call it the ‘everything bubble’: the price bubble of everything. For a processing country like Italy, which has to import almost everything, this is becoming a serious problem. What is happening is the result of three factors that add up: real, financial and logistical.

The causes

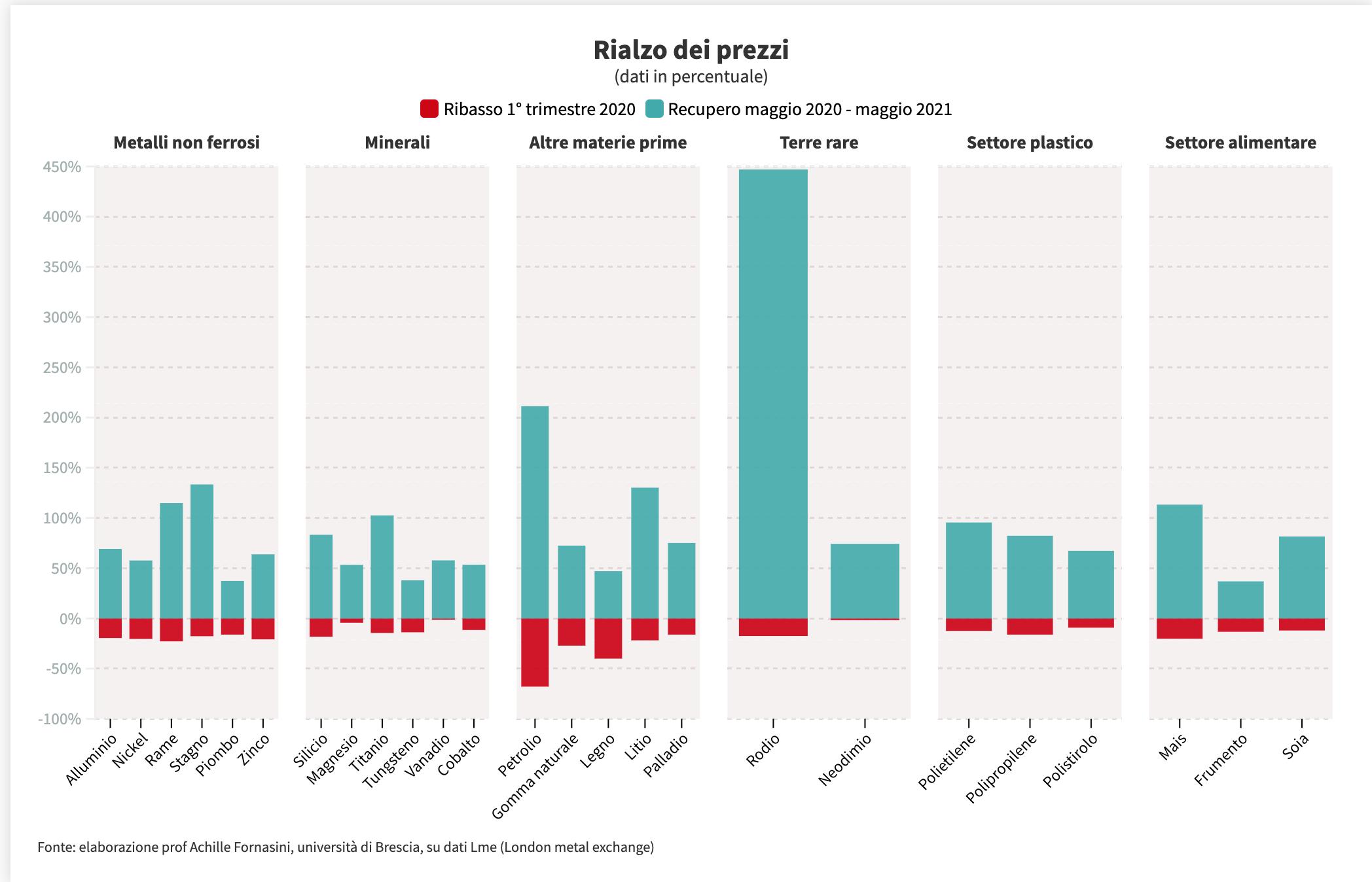

Let us start with the ‘real’ ones. In the first months of the pandemic, raw material prices fell by 20-30%. China, which has a planned economy, immediately took advantage of this to stock up, also benefiting from the fact that it had restarted four months earlier. But immediately afterwards, prices started to rise again, and now they are sky-high, because all the countries have restarted in a hurry, with warehouses on every continent empty because of the ‘just in time’ organisation (companies have got used, in order to be more efficient, not to accumulate stock) and, therefore, they now have to be replenished from scratch. Then there are causes that have to do with the financial markets. Commodities have become an attractive investment because they are priced in dollars, a weak currency at the moment, so they are convenient for those who buy them in euros or other currencies. Also: investing in government bonds gives very low returns, so you might as well put money into commodities and derivative securities linked to them. Add to this the disproportionate increase in transport costs. The Dry Baltic Index, an index summarising sea freight charges for dry and bulk products (minerals, cereals, etc.), has risen by 605% in the past year. One of the causes was the introduction of the new regulation approved by the International Maritime Organisation requiring all ships to lower the sulphur content of fuel oil: from 3.5% (mass-for-mass) from January 2020 to 0.5%. This change has meant ‘scrapping’ some ships and ‘revamping’ others, including container ships and bulk carriers transporting goods from the Americas, Africa, Asia and Australia, and the cost has been passed on in prices.

“(…) spiralling transport costs. The Dry Baltic Index (…) has risen 605% in the last year.”

Rare earths, lithium, cobalt

According to Professor Achille Fornasini, professor of financial market techniques in Brescia, ‘this situation will deflate because production levels are still lower than in 2019, so within a few months prices will fall to levels that reflect real demand’. But this reasoning does not apply to all ‘commodities’. There are in fact some commodities that are needed in quantities never used before, because they are indispensable for the two revolutions taking place in the production system: the green transition and the digital transition.

![]()

We are talking about copper, lithium, silicon, cobalt, rare earths, nickel, tin, zinc. In just one year, tin, used for micro-soldering in the electronics industry, has increased by 133%, and demand will continue to grow in the face of contracted supply. The price of copper has increased by 115%. Rhodium is a ‘rare earth’ used for electrical connections and for making catalytic converters: up 447%. Neodymium is mainly used in the production of super-magnets for lighting systems and the plastics industry. In great demand: plus 74%.

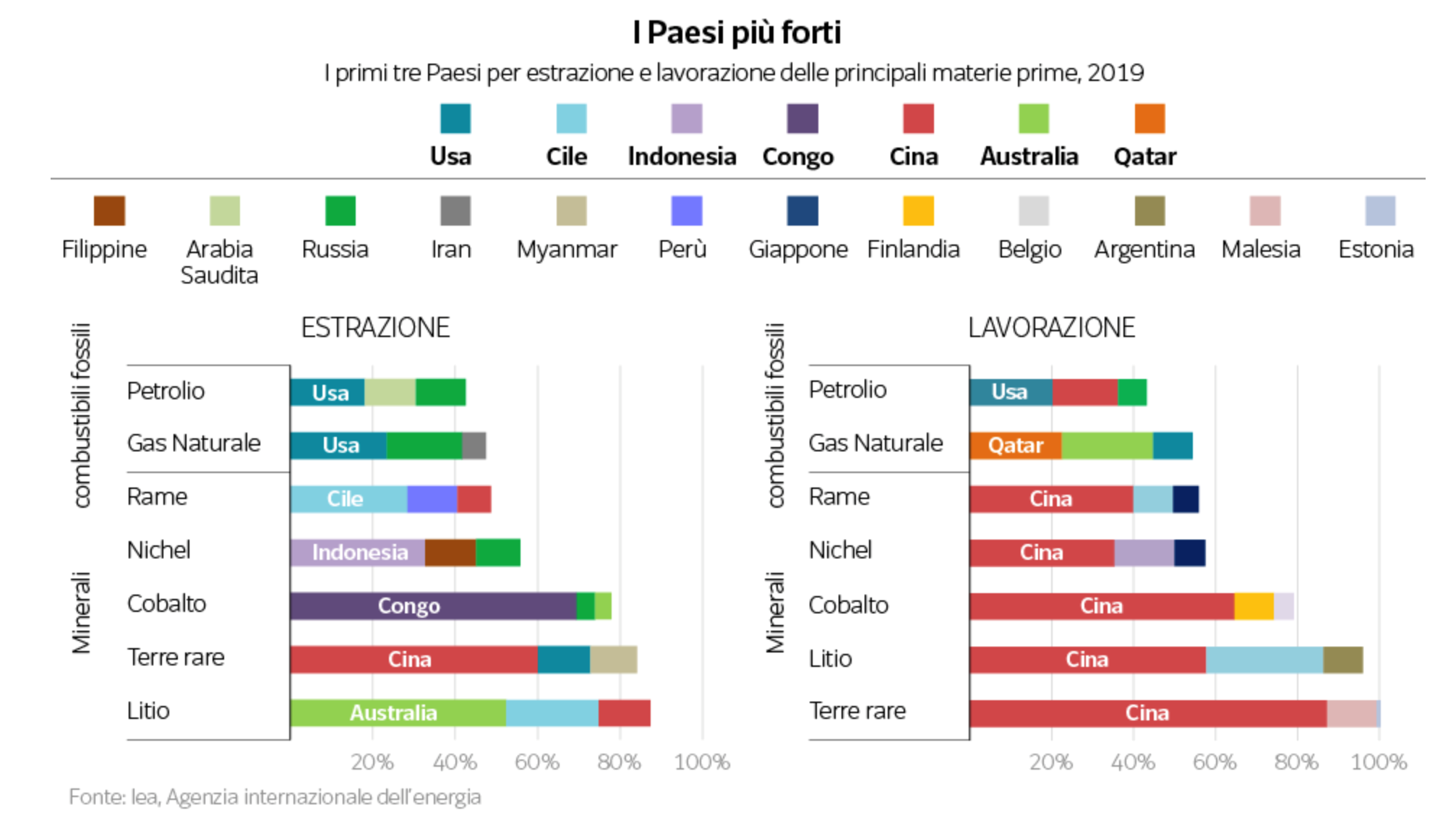

China takes the cake

Today, revenues from coal production are ten times higher than from the production of the minerals used in the transition process. But, according to the International Energy Agency, the situation will be reversed by 2040.

The most far-sighted have been the Chinese. At home they are great extractors of copper, lithium, rare earths. And what they lack they go and get in the producing countries: nickel in the Philippines and Indonesia, in Congo they own the main cobalt mines. Minerals that they then process directly in the mother country. According to Benchmark Mineral Intelligence, a British analysis company, 80 per cent of the raw materials needed for the construction of lithium-ion batteries come from Chinese companies.

Europe increasingly in trouble

Europe increasingly in trouble

The European Commission points out that there are thirty critical raw materials, including lithium itself. For the supply of rare earths we depend on China for 98 per cent, ditto for borate from Turkey, and South Africa for 71 per cent of platinum requirements. The Commission estimates that the EU will need up to 18 times as much lithium supply for electric vehicle batteries and energy storage in 2030, and up to 5 times as much cobalt. Quantities will triple by 2050, while demand for rare earths used in permanent magnets (electric vehicles, digital technologies, wind generators) will increase tenfold.

“For the supply of rare earths we depend on China for 98 per cent, ditto for borate from Turkey, and South Africa for 71 per cent of platinum requirements.”

How we come out

Twenty years behind China, the European Union formed the Raw Materials Alliance last October. The strategy is to become more autonomous by focusing on three objectives. The first is to promote the mining of metals in Europe using advanced technologies. The demand for lithium, for example, can be met 80% internally by 2025. Today, strategic metals mined in Europe, such as lithium, are mainly processed in China. The processing process, on the other hand, will have to be developed rapidly at home. Six innovation centres have been set up, including one in Rome, with the aim of implementing the sector by creating partnerships between companies and between companies and universities. In Italy we have some cobalt in Sardinia and at Punta Corna, in Piedmont, where there is also nickel; while in Gorco, in the province of Bergamo, there is zinc. Of course, these are invasive activities. But it will have to be decided once and for all whether to leave them in the hands of countries that, besides making us economically dependent and exposed to price blackmail, have less strict rules than ours and use more polluting technologies.

The harms of non-recycling

Second point: increase recycling of precious metals. We have shown that we can do this with paper and aluminium, but not with electronic waste, starting with mobile phone batteries. As for recycling batteries, we send the bulk to China, which now dominates the world market, and we pay them to do this. Then from China we buy new batteries and goodnight. A strategic mineral is cobalt. From the data of the European Institute of Innovation Technology Rowmaterials: the EU pays to import 40,000 tonnes of it every year, half of which ends up in products that remain within the EU, where end-of-life recycling is minimal, when instead a percentage that can be close to 50% is recoverable.Moreover, we throw away thousands of tonnes of used computers and mobile phones in landfills at home and in Africa. This is irresponsible behaviour which, on the one hand, causes gigantic pollution and, on the other hand, disfigures the environment because it makes it necessary to extract new cobalt. That is why we must focus on collection, storage and recycling chains, which are completely lacking today. Third point: build a common foreign and industrial policy to obtain the concessions of the minerals we do not have.

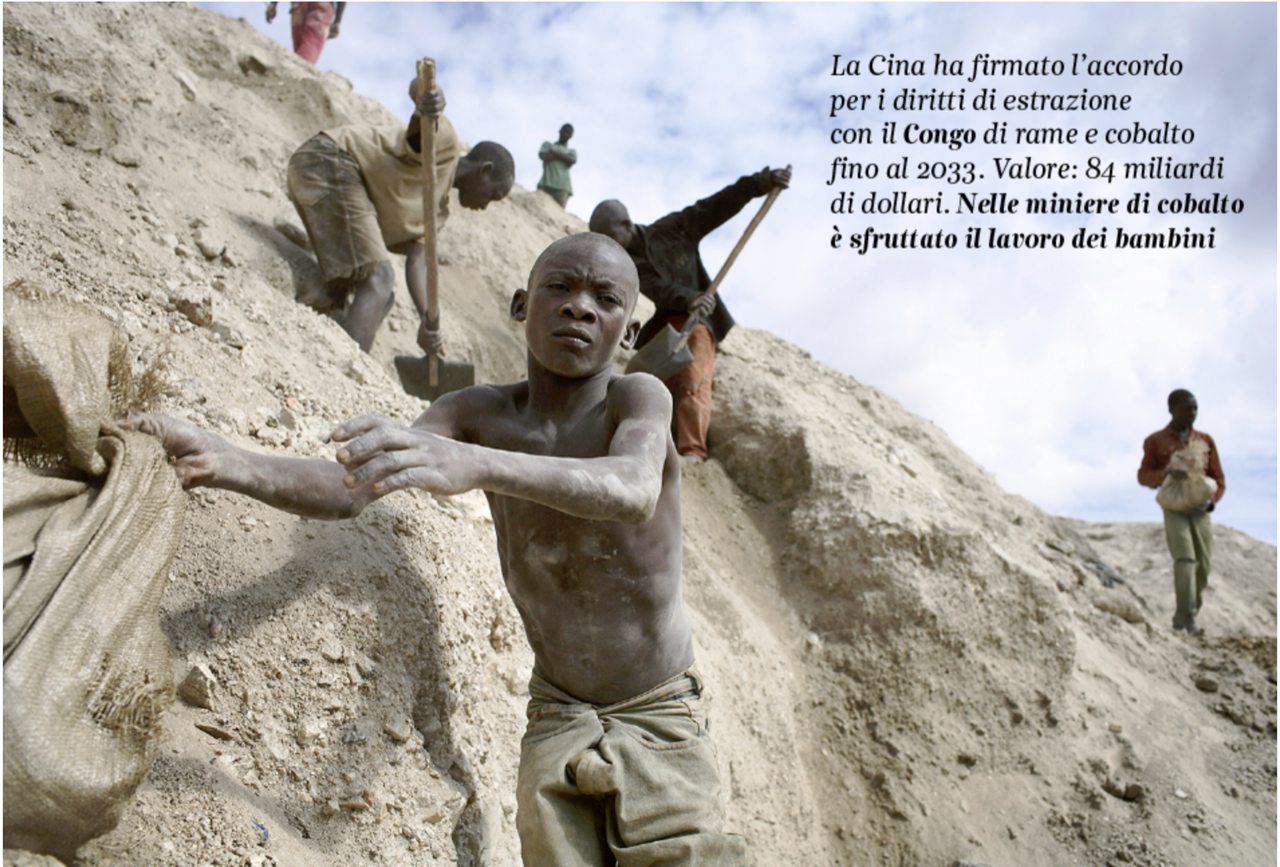

Sicomines, a consortium of Chinese state-owned companies, signed an agreement with Congo in 2008 for copper and cobalt mining rights until 2033, worth an estimated USD 84 billion. In return it pledged to invest $6 billion in the country’s infrastructure and about $3 billion in mining. For years, child labour has been scandalously exploited in those mines, causing the indignation of half the world. Providing better conditions is not only a necessity. It is a duty.

dataroom@rcs.it[/vc_column_text]