… Esselunga’s best competitor is Iper la grande I (Finiper), but also Lidl and Eurospin.

A separate argument should be made about Tigros and Iperal, which, in fact, are somewhat smaller Esselunga stores with less extensive and deeper assortments, but where it is probably easier to shop in less time. To this must be added the presence of bistros with good value for money.

And then, you must allow us, the presence of a convincing fruit and vegetable department. This is because, beyond the performance of the grocery-salon, the main reason for shopping in a supermarket remains the fruit and vegetables, whether one likes it or not.

It is a pity, dear Luigi, that the fruit and vegetable departments are – in general – increasingly pitiful and it is a race to see who is ‘less worse’ (although Coop Fi might be an exception)

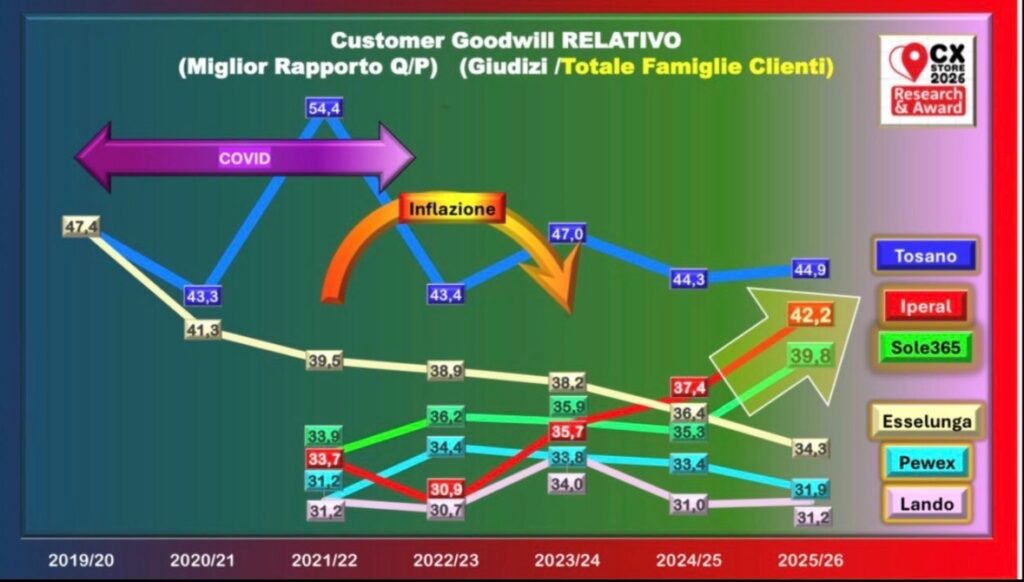

Below: Daniele Tirelli’s analysis of Goodwill – corporate goodwill – related: Localism. Here is the other key word emphasised by the seventh edition of CX Store Research. Esselunga’s declining trend is what attracts attention more than any other fact: a brand that for decades represented the absolute benchmark of quality in Italian food retail is now seeing its Relative Goodwill eroded not by a stronger national competitor, but by a constellation of local brands that surround and undermine it – each in its own catchment area – with value propositions credible enough to intercept the incumbent’s customer, i.e. the one who appreciates Esselunga’s quality but sees an overpricing…

Thanks to Mario Gasbarrino

Edited 12 May, updated 24 May 2026