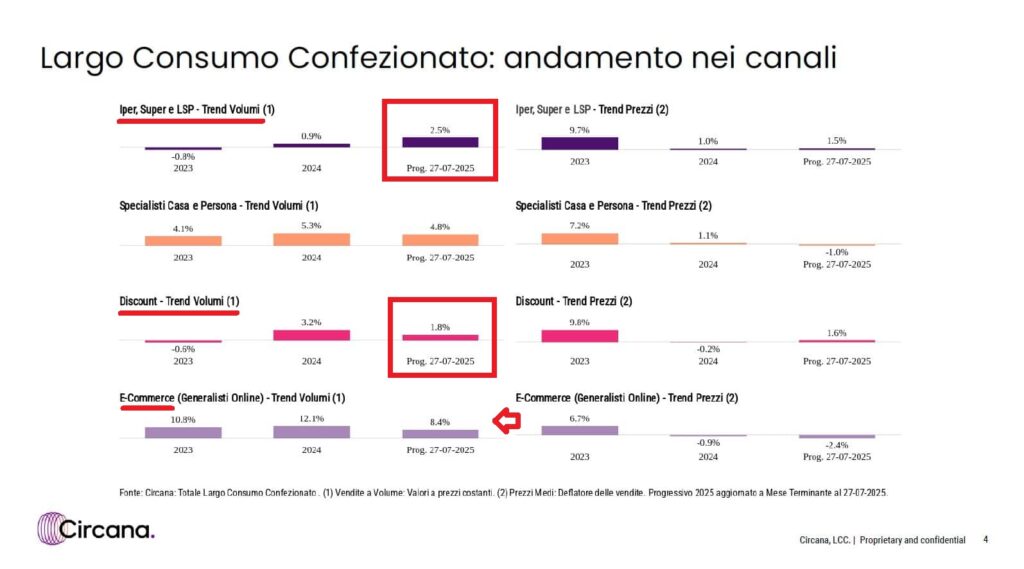

“From 2019 to 2023, their [the discounters’] turnover grew at an average annual rate of 9.3 per cent, compared to 5.7 per cent for the other operators”(we reported this here). Then there was aturnaround: the growth in volume of the hyper and super channel exceeded (2.5%) that of the discounters (1.3%) . E-commerce was very good at 8.4% (see first table below).

Circana data show how, after 9.1% in 2023, value sales grew more slowly in 2024 ( 2.4%) to consolidate in 2025 with a further 3.7%.

The significant novelty is that, unlike the previous two-year period, growth is no longer just an effect of prices, but is accompanied by a recovery in real demand: volumes, in fact, declining by 0.5% in 2023, turn positive in 2024 ( 1.8%) and accelerate in 2025 ( 2.3%). Supporting this rebalancing is also the dynamics of prices, which after a 9.5% surge in 2023, stop at 0.6% in 2024 and travel at 1.4% in 2025, returning to physiological levels.

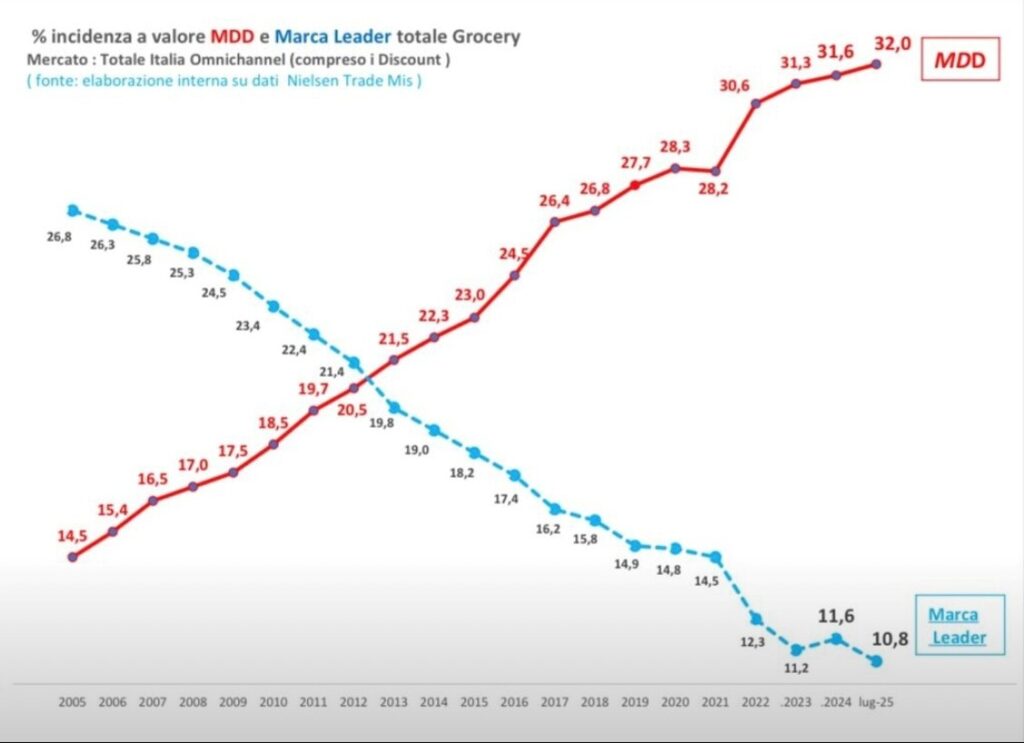

Below: one of the factors in the recovery of the Iper Super channel (in which there are also superstores) was probably the strength of the private label, which expressed convenience, and which is beating the leading brands (such as Barilla or Coca-Cola, to give examples, see the second table). A comparison between the different channels – hyper/super/superstore ‘versus’ discounters – on prices is unfortunately not possible to date.

p.s.: looking at the ISTAT data, the drop in volumes highlighted a few days ago, seems to affect only small retailers, not the GD (page 3).

Note that ISTAT has only been using barcodes since 2020 and that not all retailers use them.

Compiled 7 September, updated 8 September 2025