Article from 2010, updated 24 December 2025

For the list of products see PDO and PGI on Wikipedia.

Very often when choosing a product we are inclined to give preference to those bearing a ‘quality’ label, against which we are also willing to spend that little bit extra.

But when we rely on a PDO (Protected Designation of Origin) or PGI (Protected Geographical Indication) label, do we know what we are buying?

Both marks – PDO (Protected Designation of Origin) and PGI (Protected Geographical Indication) – derive from the application of EEC Regulation 2081/92 promoted by the European Community, with the aim of protecting those traditional agri-food productions linked to a particular geographical territory, as a consumer guarantee.

But even if these two marks appear identical to each other, were it not for the different wording that characterises them, they actually conceal very different production situations that are worth knowing and evaluating.

The difference between the two is therefore substantial and, taking a cue from recent news events, allows us to understand why our bresaola – produced using almost only Brazilian or Argentinian meat – can be awarded the PGI mark but not the PDO mark.

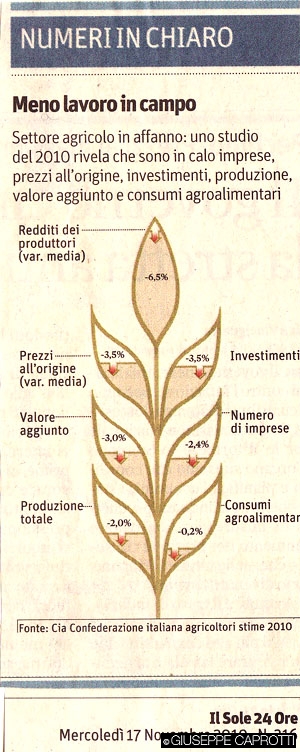

For the updated data see the end of the article: we also keep the ‘old’ data (2008) for comparison.

PDO and PGI, some figures between light and shade:

sales turnover is estimated at € 9.4 billion, of which € 7.5 billion on the domestic market

To the increase in brand recognition (15.4% in 2009, against a European average of 7.4%), which brings Italy to a leadership position in Europe with 213 products registered against 176 French and 140 Spanish, in most cases PDO or PGI products are not matched by interesting turnovers.

Eighty per cent of the turnover comes from a dozen or so big brands, which are then the same emblazoned products that cross national borders.

In descending order by production value in 2008 in sales they excel:

- Grana Padano

- Parmesan cheese

- Parma ham

- San Daniele ham

- Mozzarella di bufala campana

- Mortadella

- Gorgonzola

With almost 4 billion € (to which the margins of the respective products have to be added to arrive at consumer prices).

In Italy, the weight of the GD, as a sales channel for food products, rose from 50.2% in 1996 to 70.8% in 2009.

PDO and PGI products have become part of everyday spending as 29.1% of households say they buy them.

Unfortunately, in the overall context of PDO and PGI consumption in the large-scale retail trade, the weight of supermarkets (-1.3%) and traditional retail (-14%) declines in favour of hypermarkets (11%) and, above all, discount stores (18%).

This dynamic seems to run counter to the need to adopt policies of valorisation and unbundling from competition on the price factor that should characterise these products.

There are also several ‘grey areas’ on the origin of branded products and foodstuffs in general, here are some examples:

1) you will hardly see the words ‘foreign ham’ in restaurants, bars, shops or supermarkets, but 2/3 of the pork legs processed in Italy come from pigs bred in Spain and Northern Europe

2) 40% of the durum wheat in pasta produced in Italy comes from Canada, Mexico or the United States but few consumers know this

3) when faced with a bottle of PGI balsamic vinegar made from organically grown grapes with the label ‘produced in Italy’ few consumers will be able to distinguish between the origin of the raw material and the place of production. Many will think it is vinegar made from Italian grapes, in our peninsula.

This is not the case.

Personally, I think that only PDO should be able to bear the name balsamic vinegar.

I therefore welcome the clearer labelling for which the government and some consortia are fighting (the current campaign of the San Daniele producers is significant, see below), also because the entire agricultural sector is suffering – as the data below show – and could benefit greatly from a better valorisation of its brands.

This must happen all the more now that with the decline in cultivated agricultural land, construction is progressing and our country is becoming less and less beautiful and attractive, even for the 44 million tourists who stay here every year.

Sources: Ismea, Nomisma, Coldiretti, Censis- Swg

Data from the year 2016 (published by Ismea in 2017)

The turnover, from 2008 to 2016, has thus risen by 36.4%, which means 4.5% – on average – every year. Much more than, for example, food sales on the Italian market have expressed

The defence and promotion of PDO and PGI products is therefore very important for Italian agriculture, and not only.

Ismea-Qualivita report: in 2024 184,000 operators and 864,000 workers in the food and wine sector. 48% of supply chains have felt the negative effect of US duties and 61% of consortia have launched market diversification strategies

Below: publicity for the consortium of PDO Parma ham (2025), more is needed to relaunch the sector!