[vc_column_textDrafted 20 June, updated 30 June 2025

By Giuseppe Caprotti, Small shops (internal document, 2002)

In 2002 I wrote an internal document to start a reflection on the future of food retail. In those pages I warned my father against the risk of focusing exclusively on superstores, arguing that small shops were more profitable, better suited to Italian squares and closer to people’s real needs. Instead, my father chose another path: he drew up a business plan centred exclusively on the superstore model.

I talked about this in my book Le Ossa dei Caprotti from page 245 to page 247.

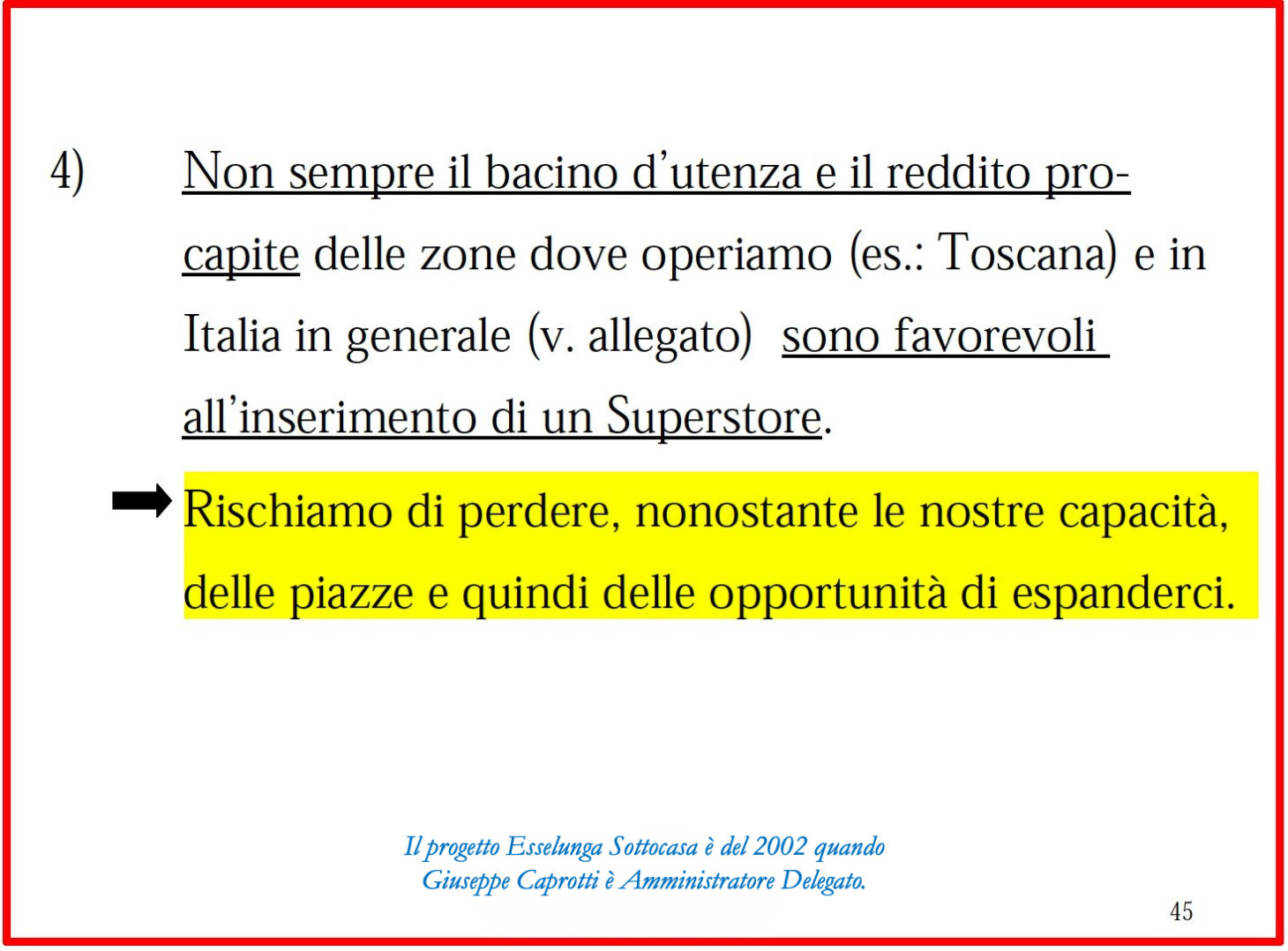

I had carefully observed how small formats, if well positioned in the urban fabric, could become not only a garrison of proximity, but also a strategic lever to deal with an ageing population, market saturation and the fall in the number of members per household. Today there are still 7 Esselunga Sottocasa but we could have set up 83.

I would like to thank Pierluigi Stoppelli for having recently shared that document, which today – more than 20 years later – still looks very relevant.

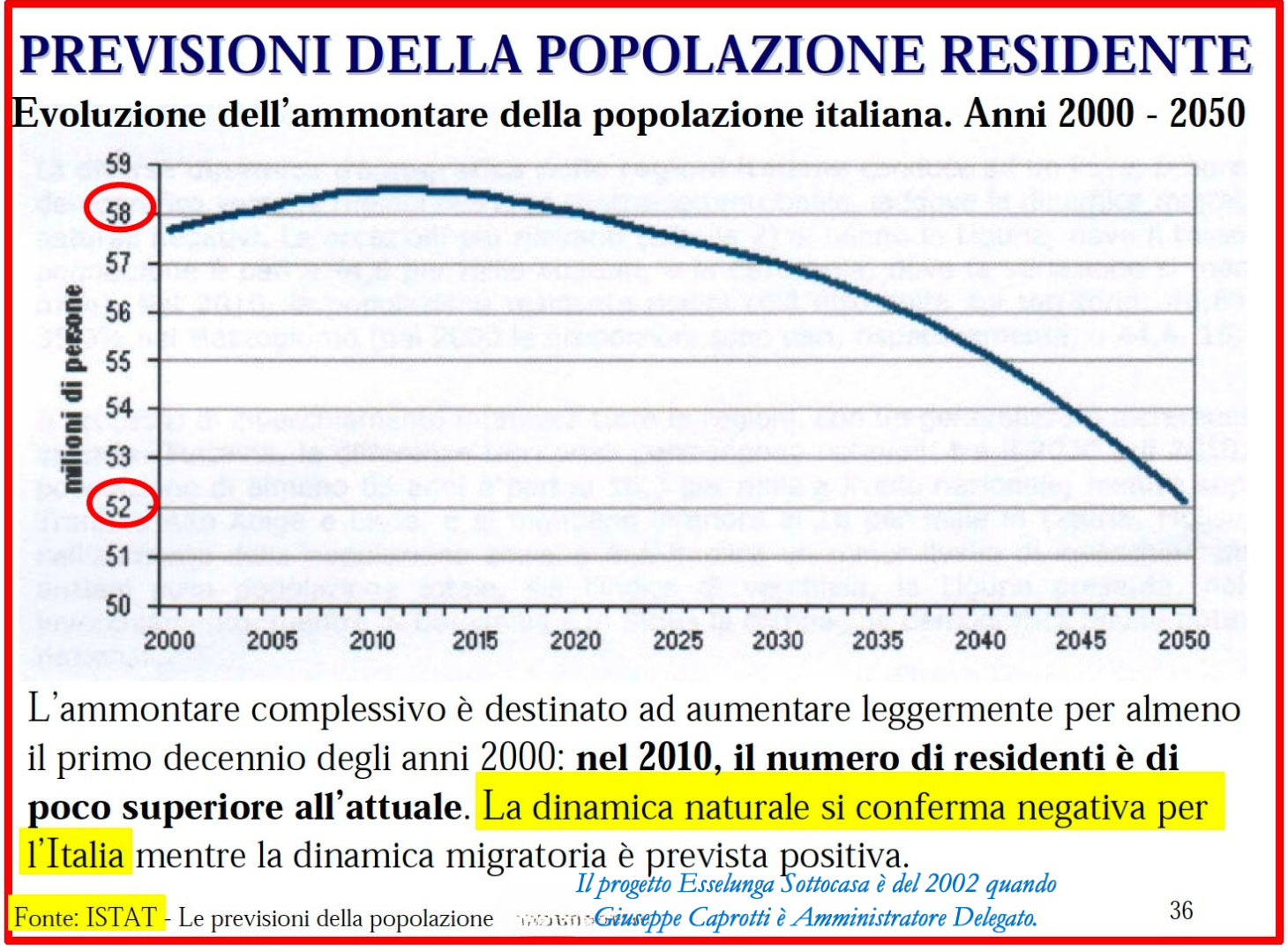

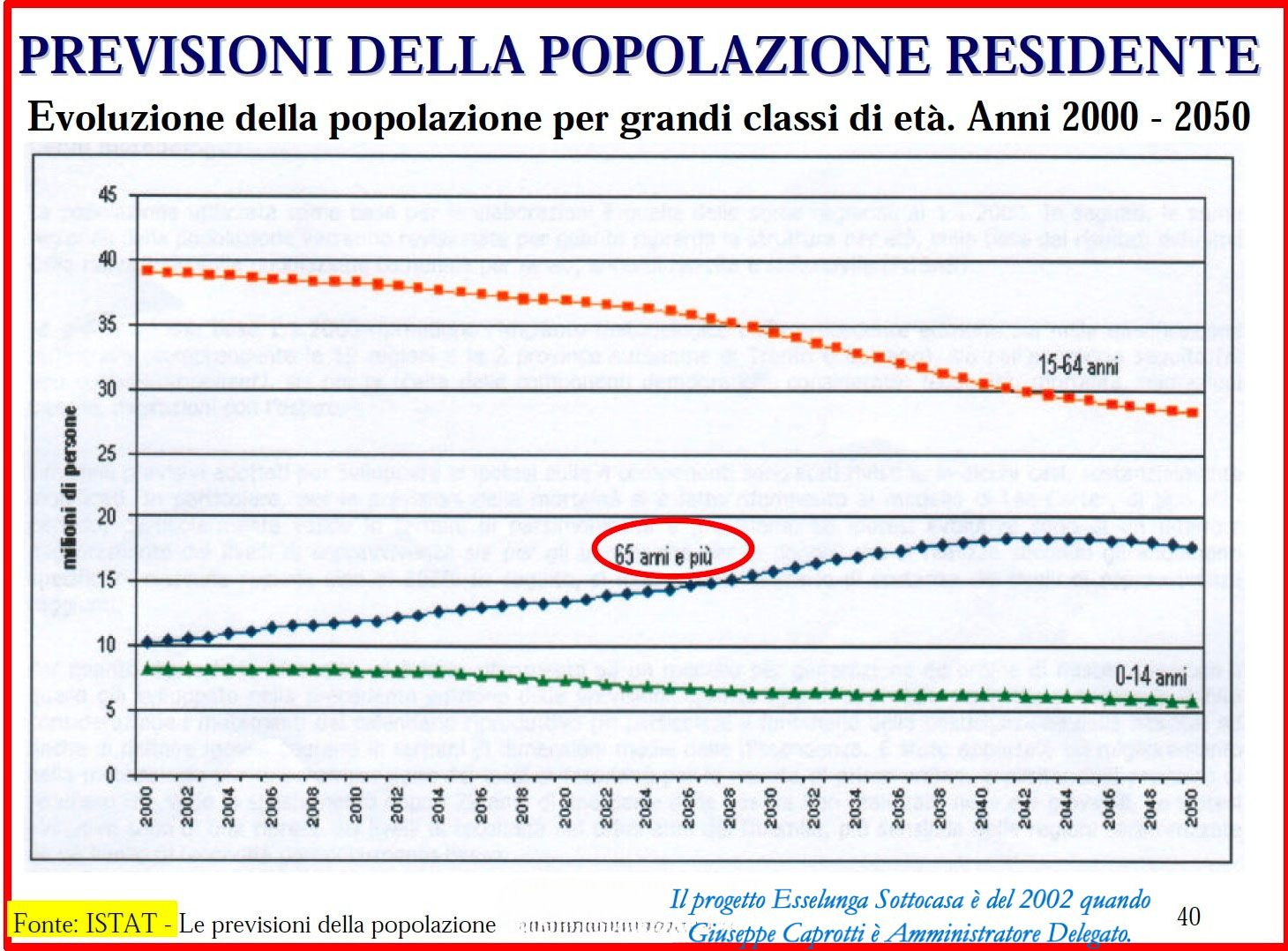

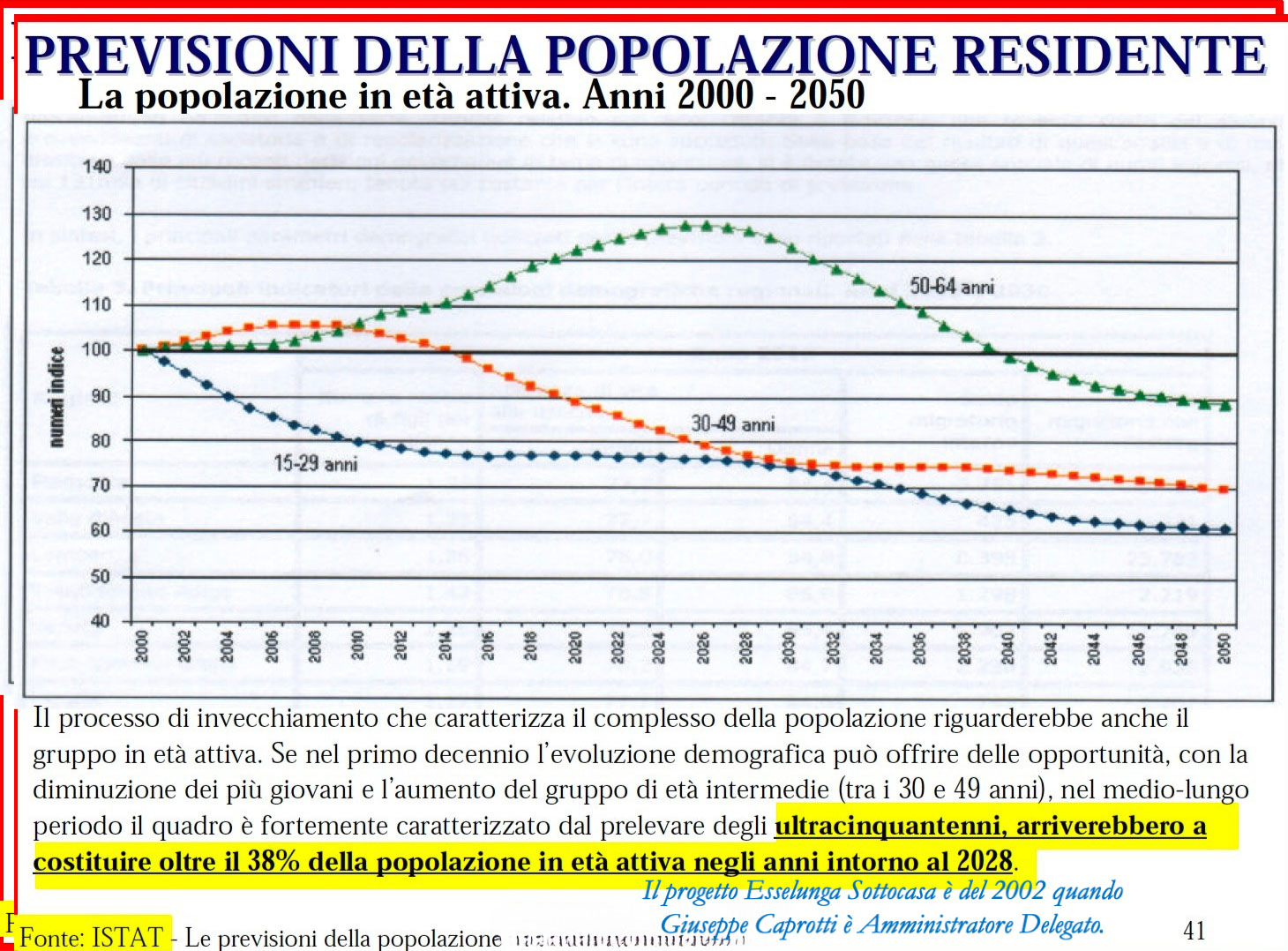

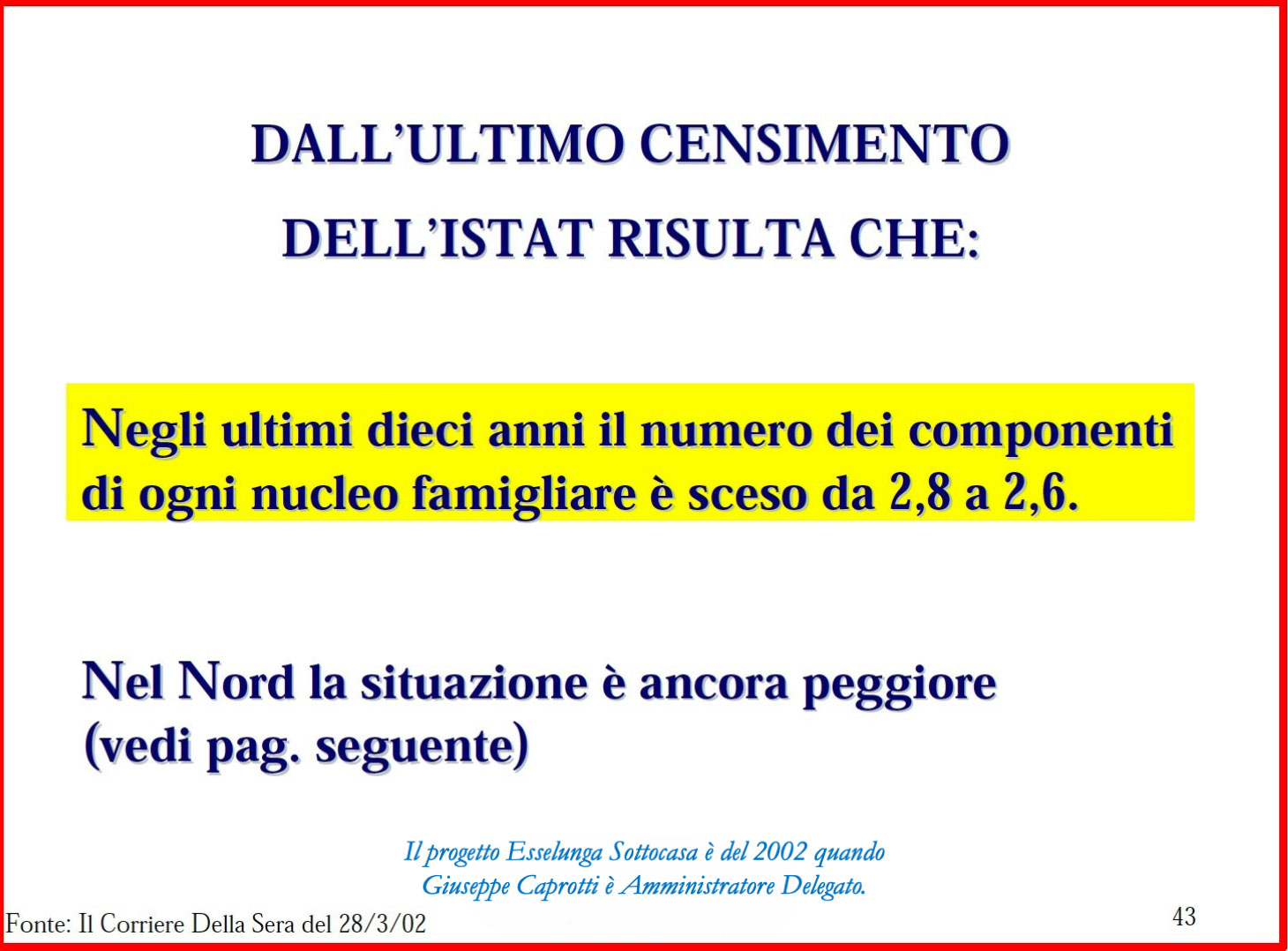

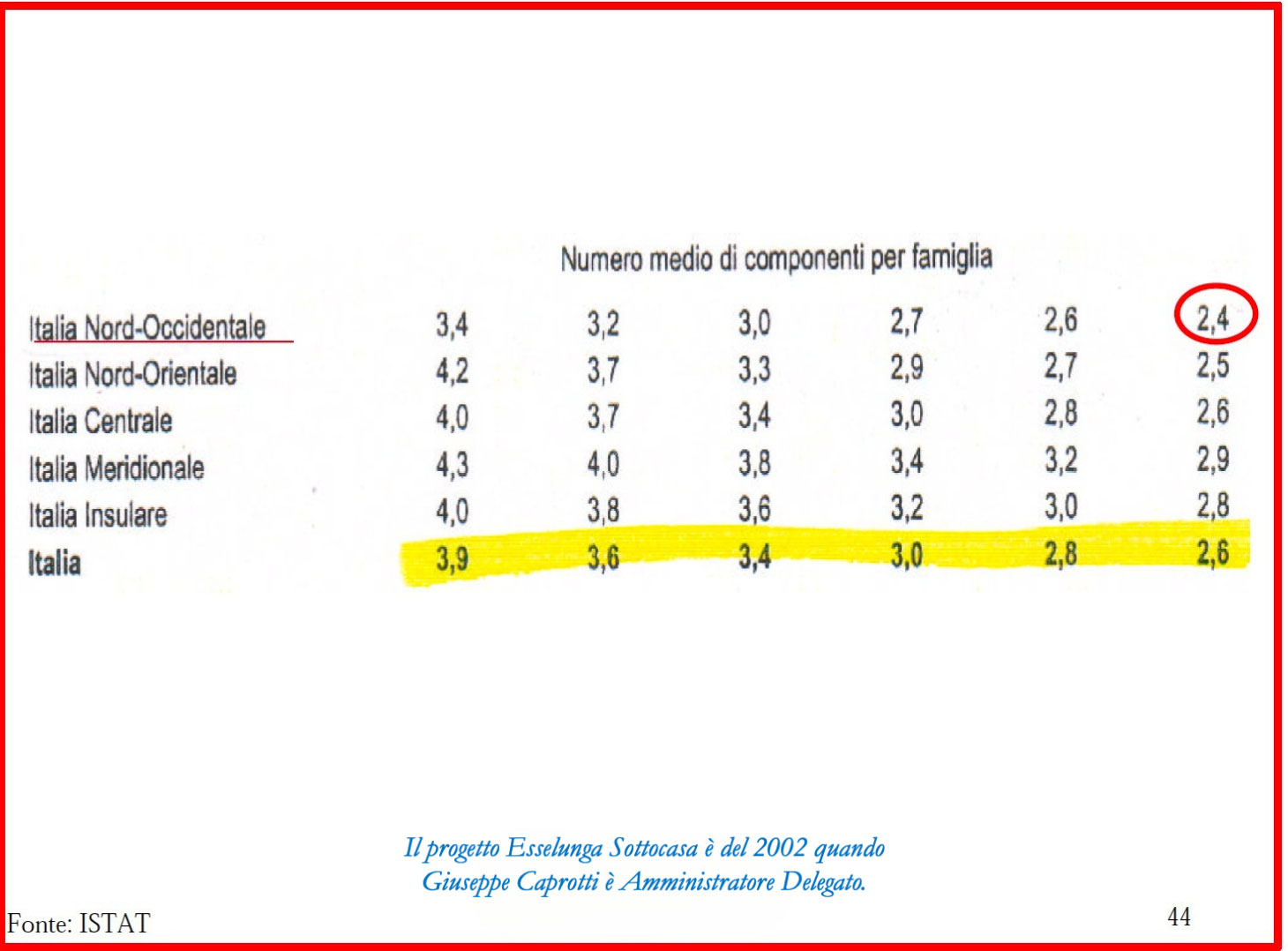

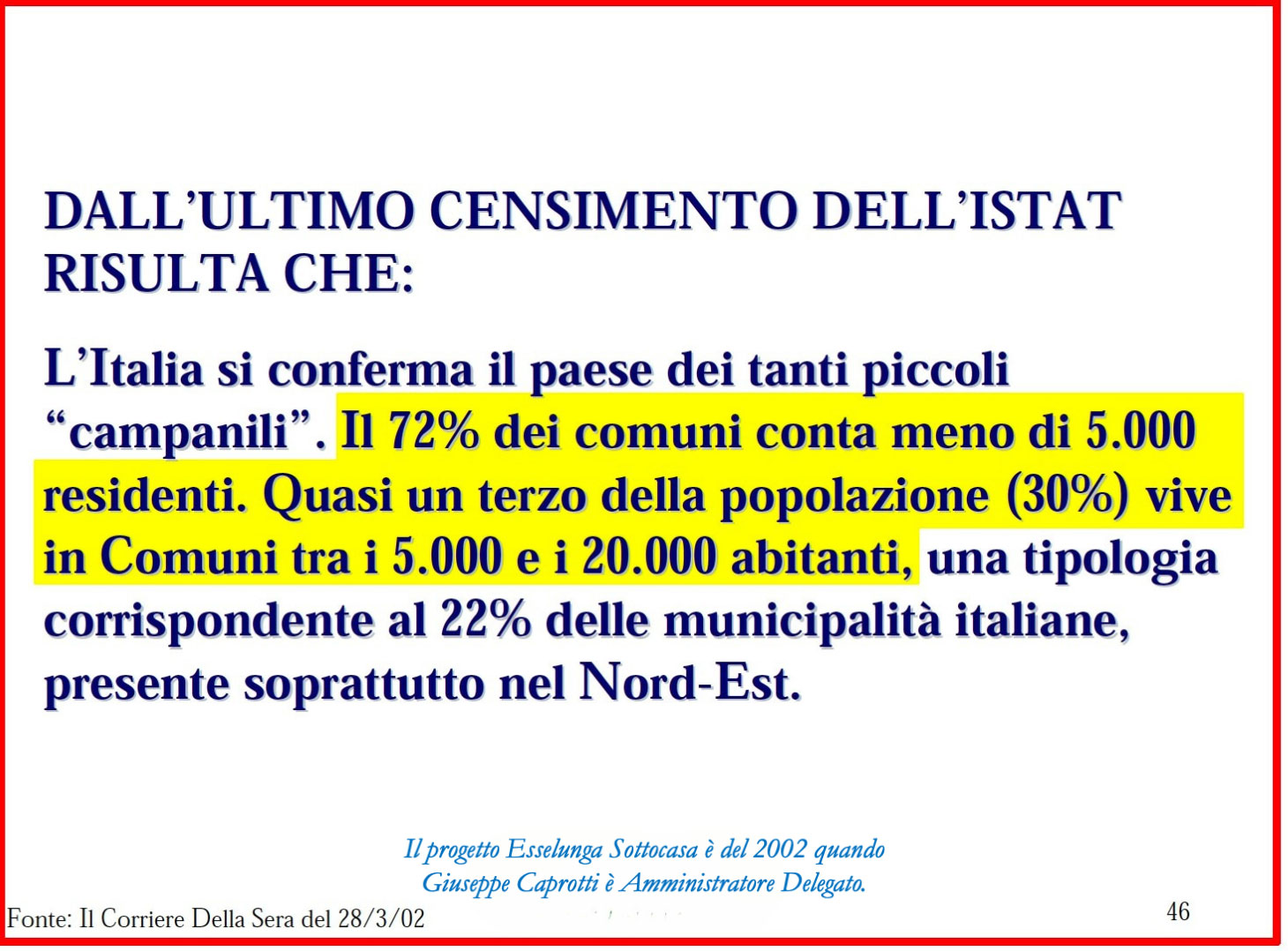

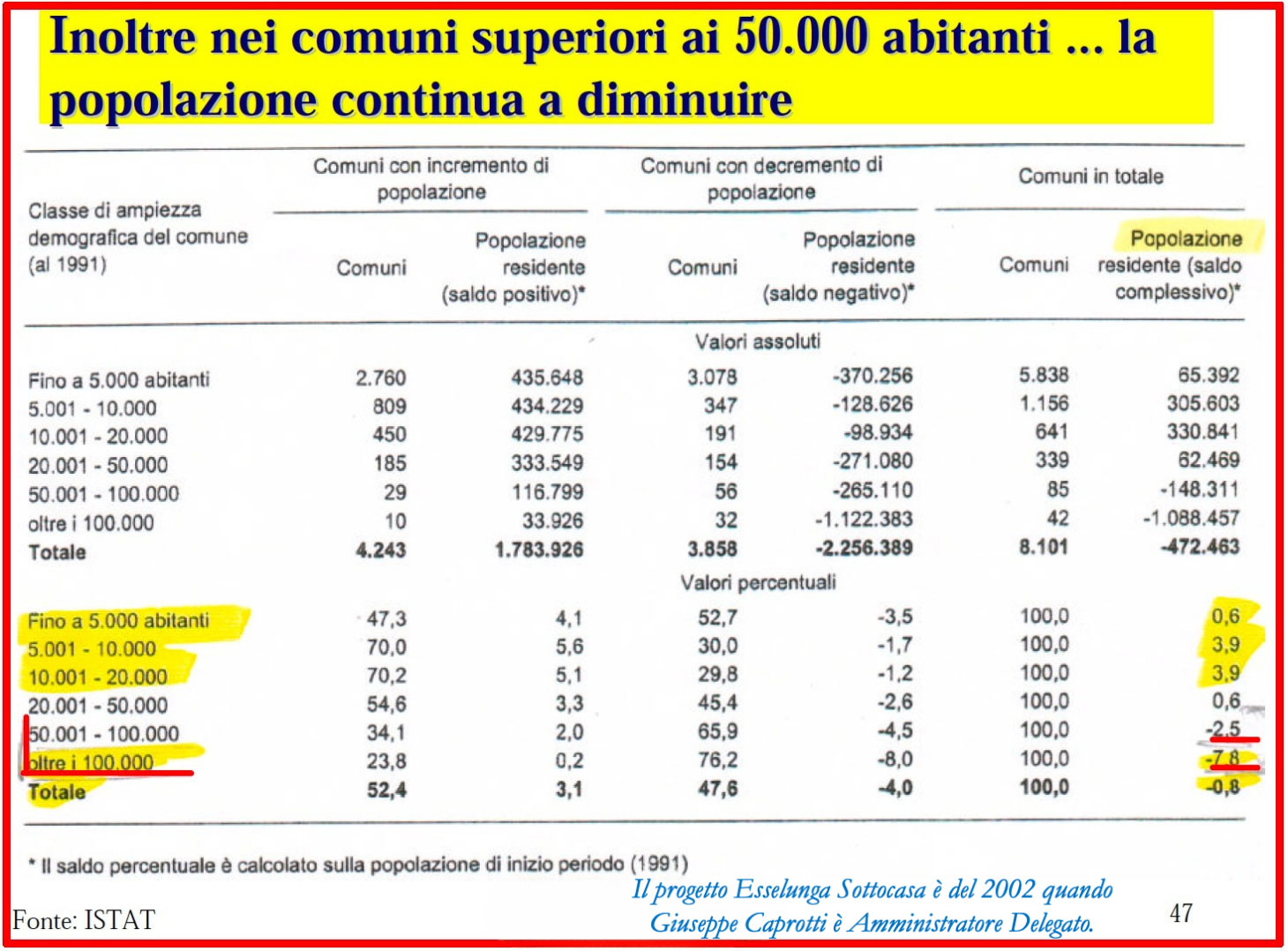

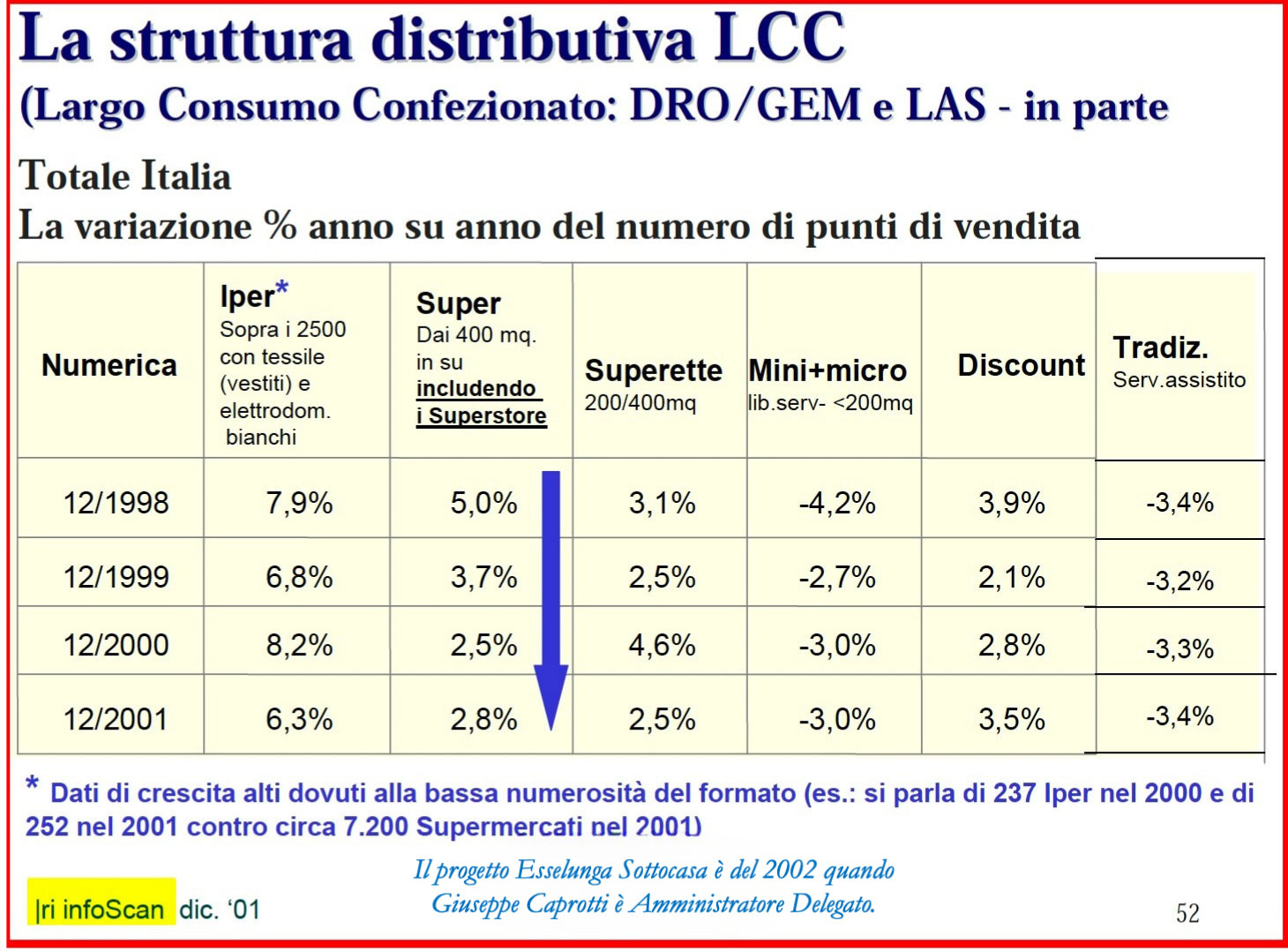

In a demographic context with consumption habits increasingly oriented towards convenience, proximity and sustainability, the proximity format is regaining centrality in the food retail scene.

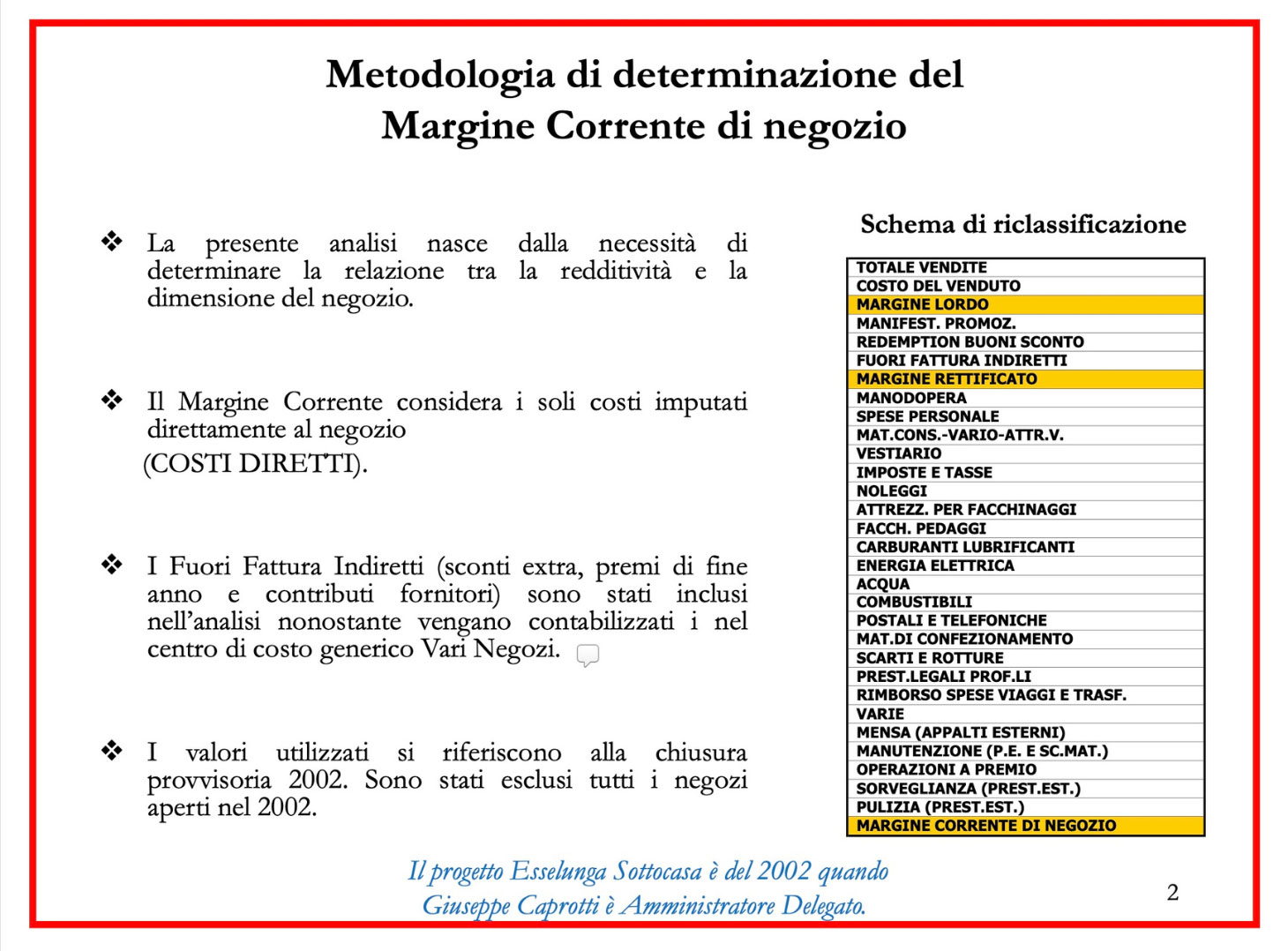

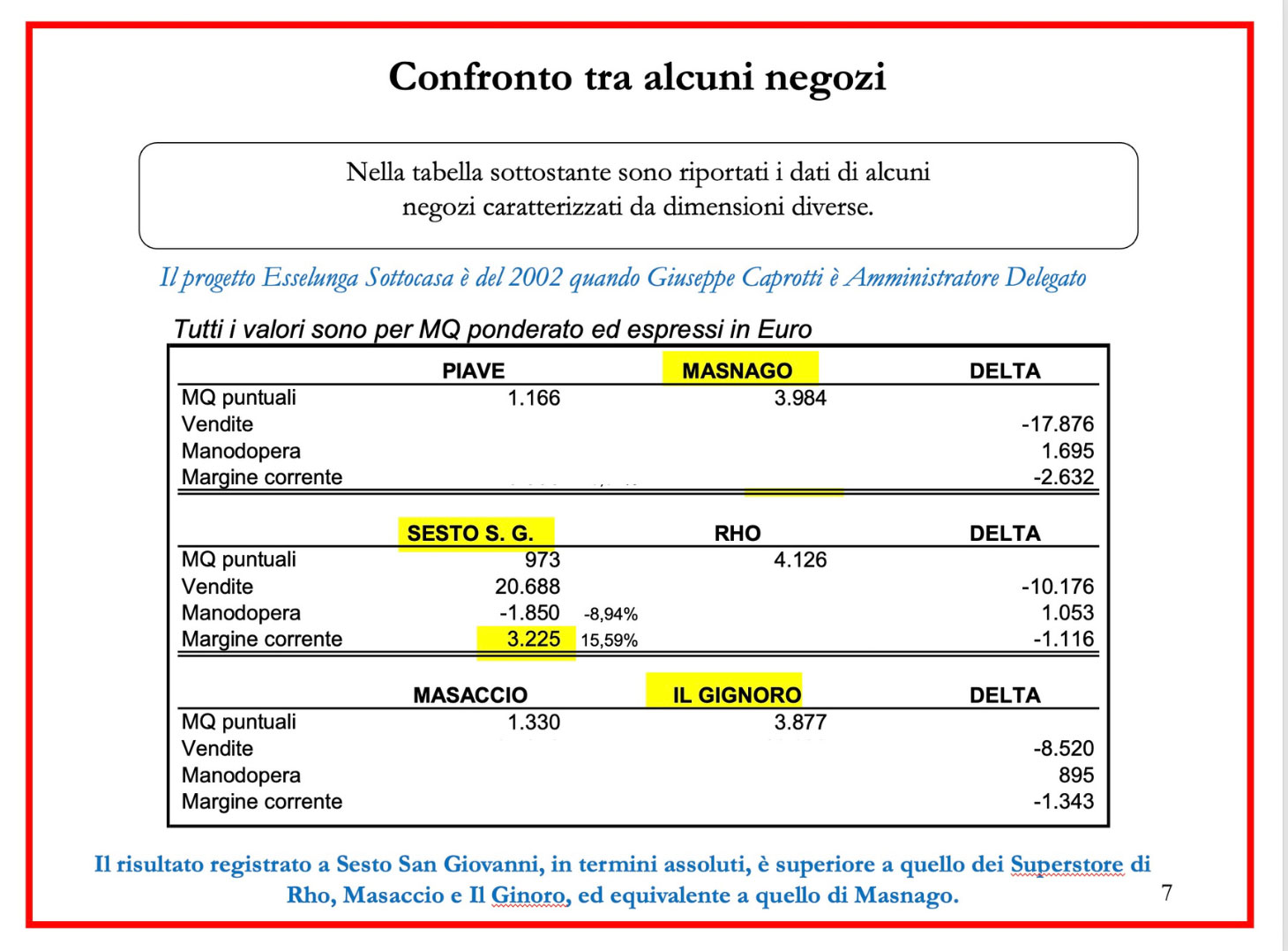

The study, based on provisional closure data from 2002 and excluding new openings in that year, analyses in detail the current margins of the shops, considering only the direct costs attributable to the individual shops (e.g. labour, utilities, consumables, maintenance).

There are three key indicators:

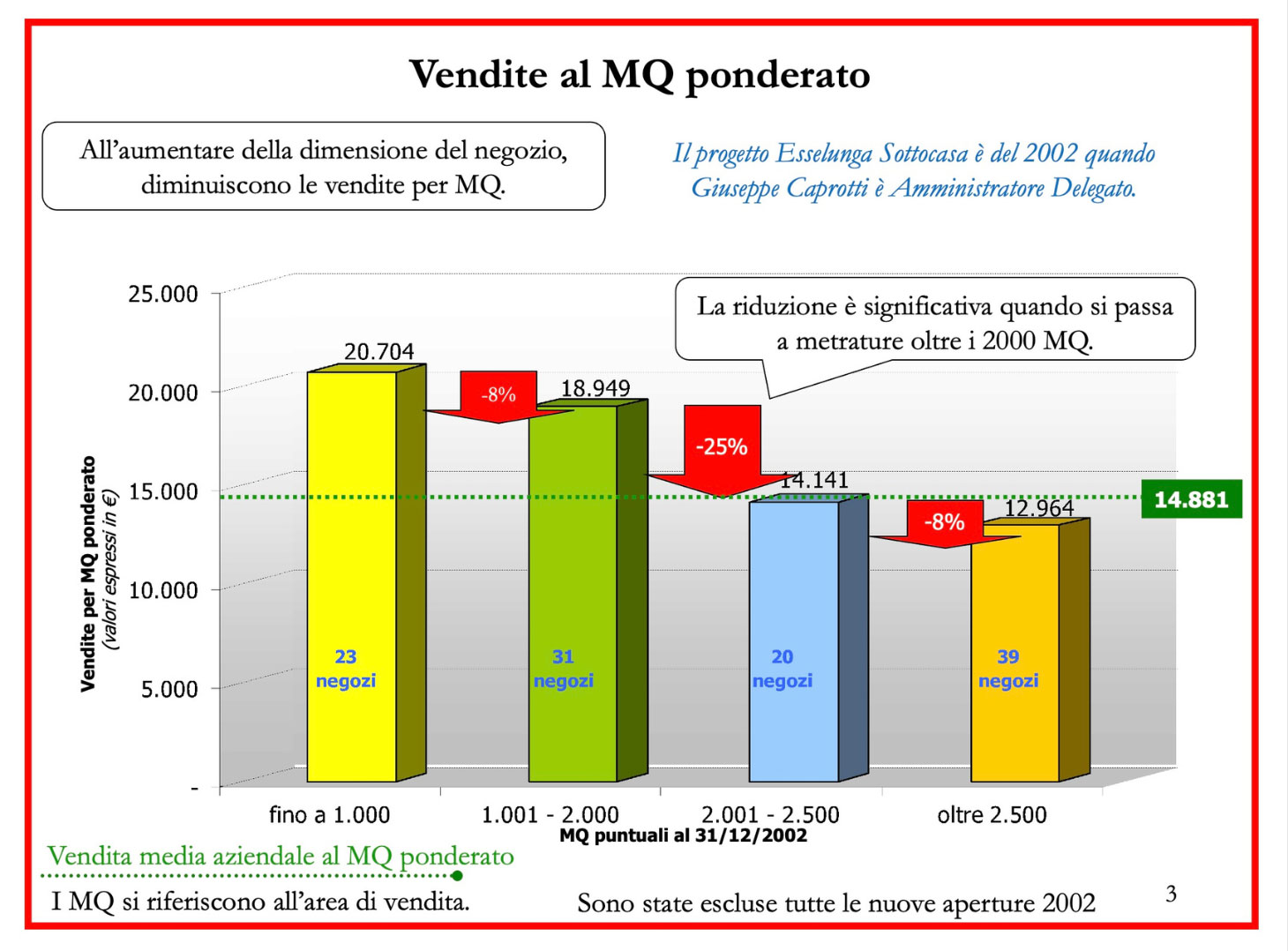

- Sales per square metre (MQ)

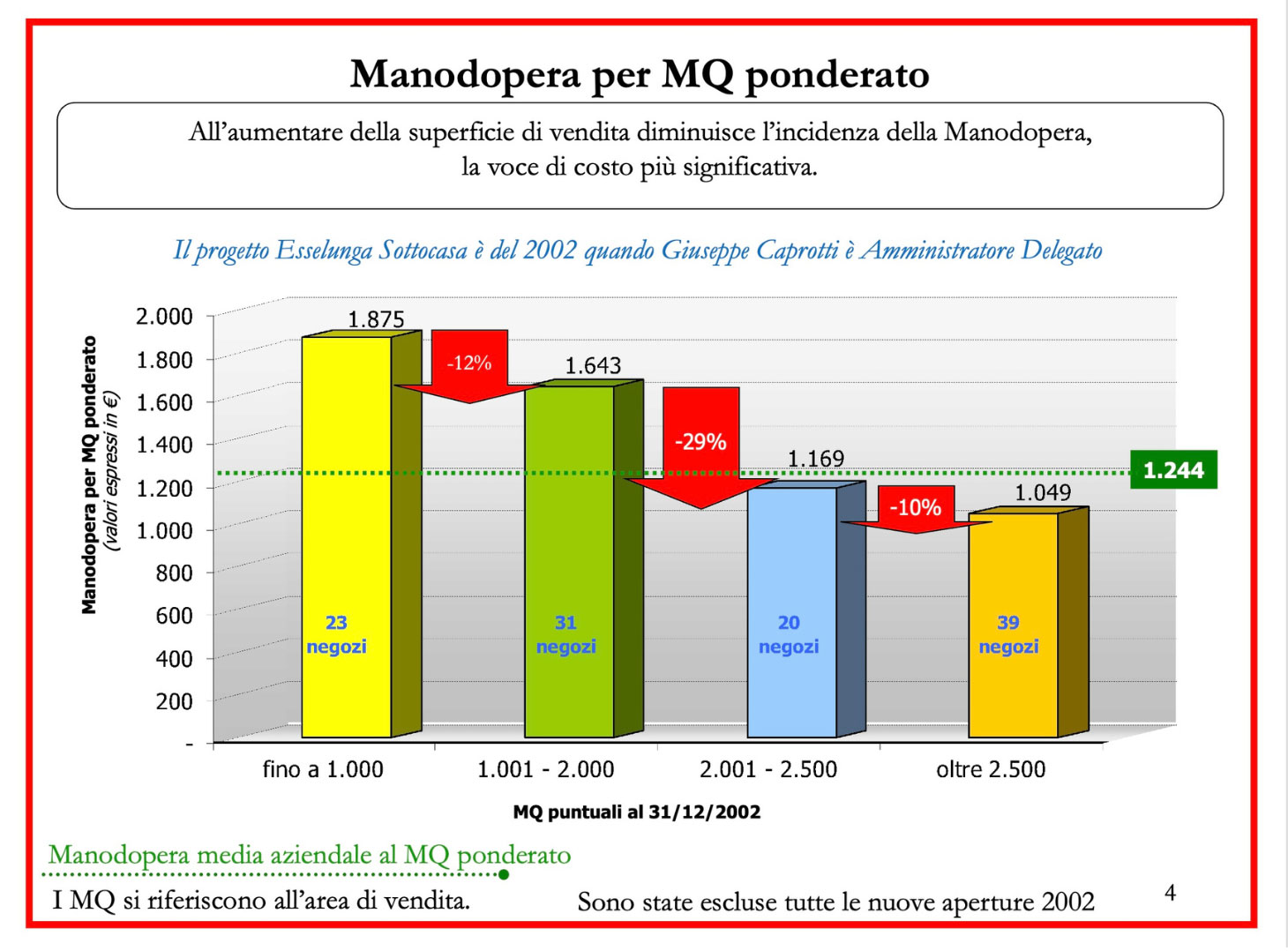

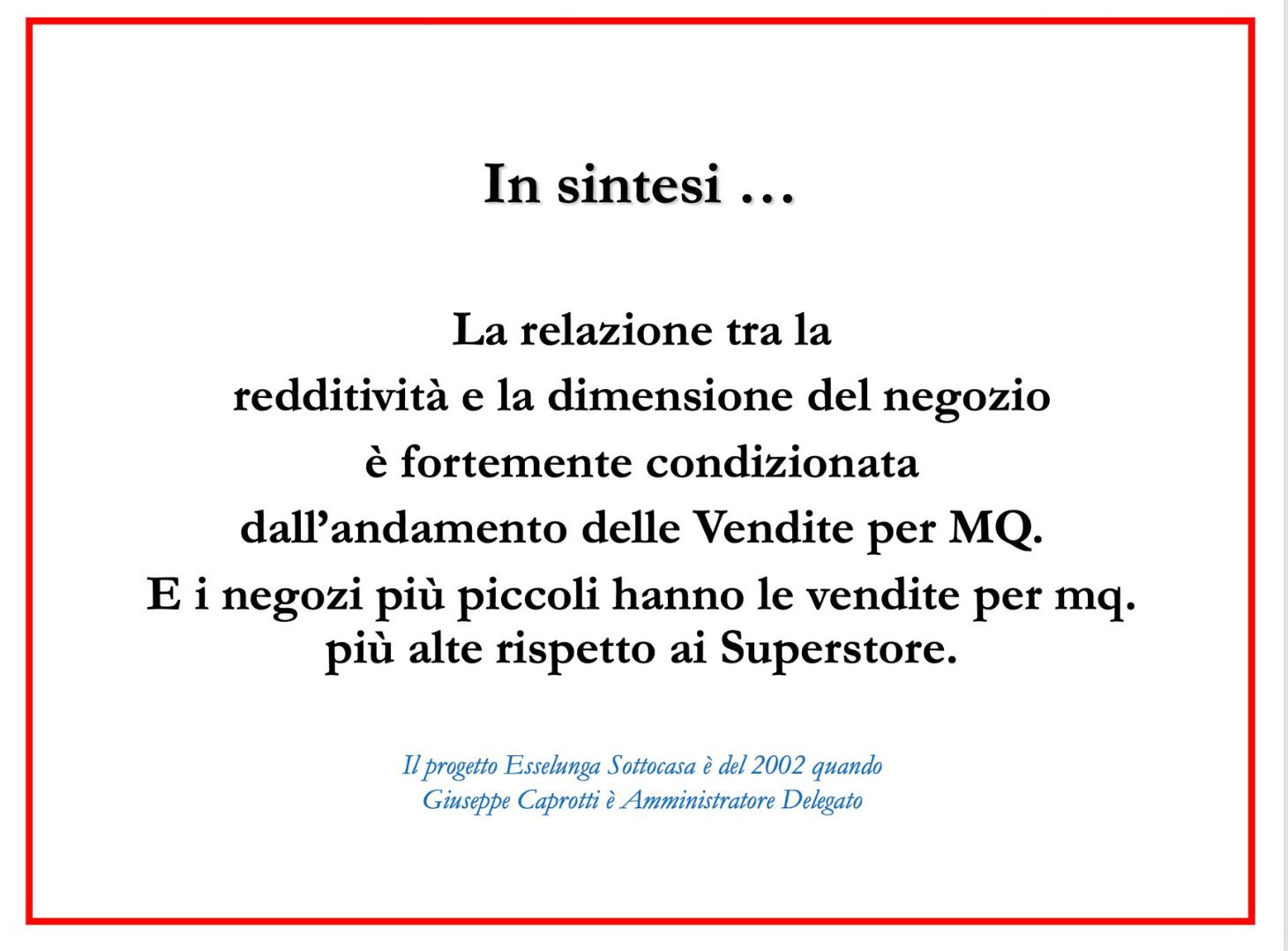

Shops with a sales area of less than 1,000 sq.m. show significantly higher sales per sq.m. than sizes above 2,500 sq.m. (more than 20,000 € vs. about 13,000 € per sq.m.). The decline is already evident above 2,000 SQM. - Labour per SQM weighted

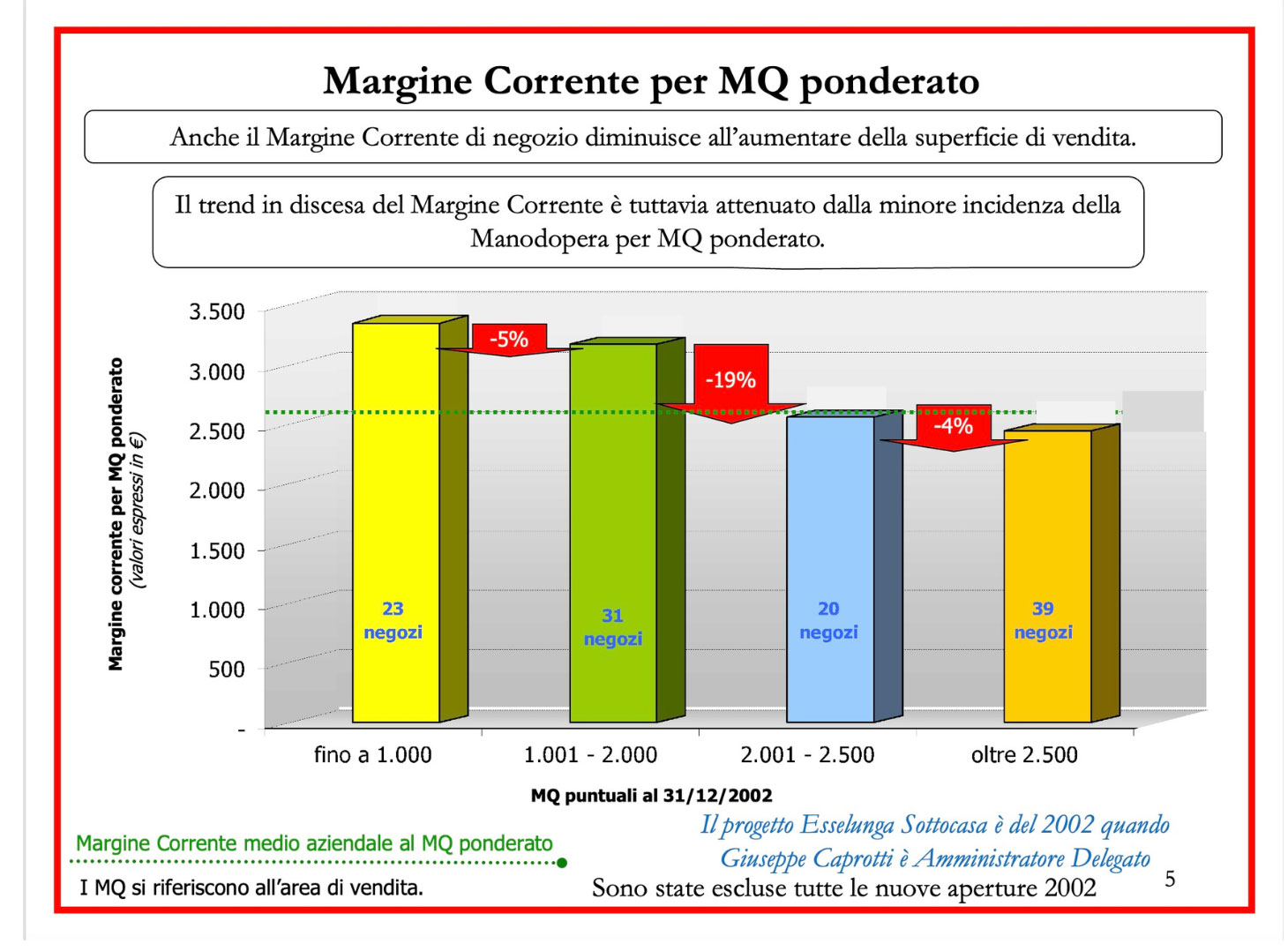

If it is true that in larger shops the incidence of labour per SQM decreases (scale effect), it is also true that this item is still significant and does not close the gap generated by the drop in sales. - Current margin per SQM

Net profitability (net of direct costs) also decreases as the sales area increases.

A concrete example helps to clarify the effectiveness of the model:

Sesto San Giovanni (SQM: 973) now owned by Carrefour, had sales per SQM: €20,688, current margin per SQM: €3,225

Despite their small size, outlets such as Sesto San Giovanni, Via Masaccio in Florence and Viale Piave in Milan recorded margins equal to or even higher than those of much larger superstores such as Masnago (VA), Rho and Il Gignoro (FI). This result was achieved thanks to higher sales per square metre, leaner operational management and customer loyalty, favoured by proximity.

To be even more precise, the current margin of Sesto San Giovanni was equal to that of the ‘flagship of the group’, the Masnago superstore.

As the slides in this article also show, the strengths of this format are many: from managerial simplicity to logistical agility, from the ability to integrate in urban contexts to greater accessibility for an ageing population. Obviously, the format also had the advantage of being able to compete – with a higher quality of fresh produce – with the discount stores, which are now advancing towards the centre of Milan.

The small shop is not a nostalgic return to the past, but a concrete, modern and intelligent response to today’s needs. It combines efficiency and profitability with the ability to build relationships of trust with the local area.

Proximity shops are perfectly suited to the Italian urban structure: in smaller towns they are the only truly sustainable solution, while in large cities, such as the centre of Milan, the small format is often the only logistically and economically viable option.

Rereading those pages today means rediscovering a vision that had grasped, well in advance, signals that have now become evident.

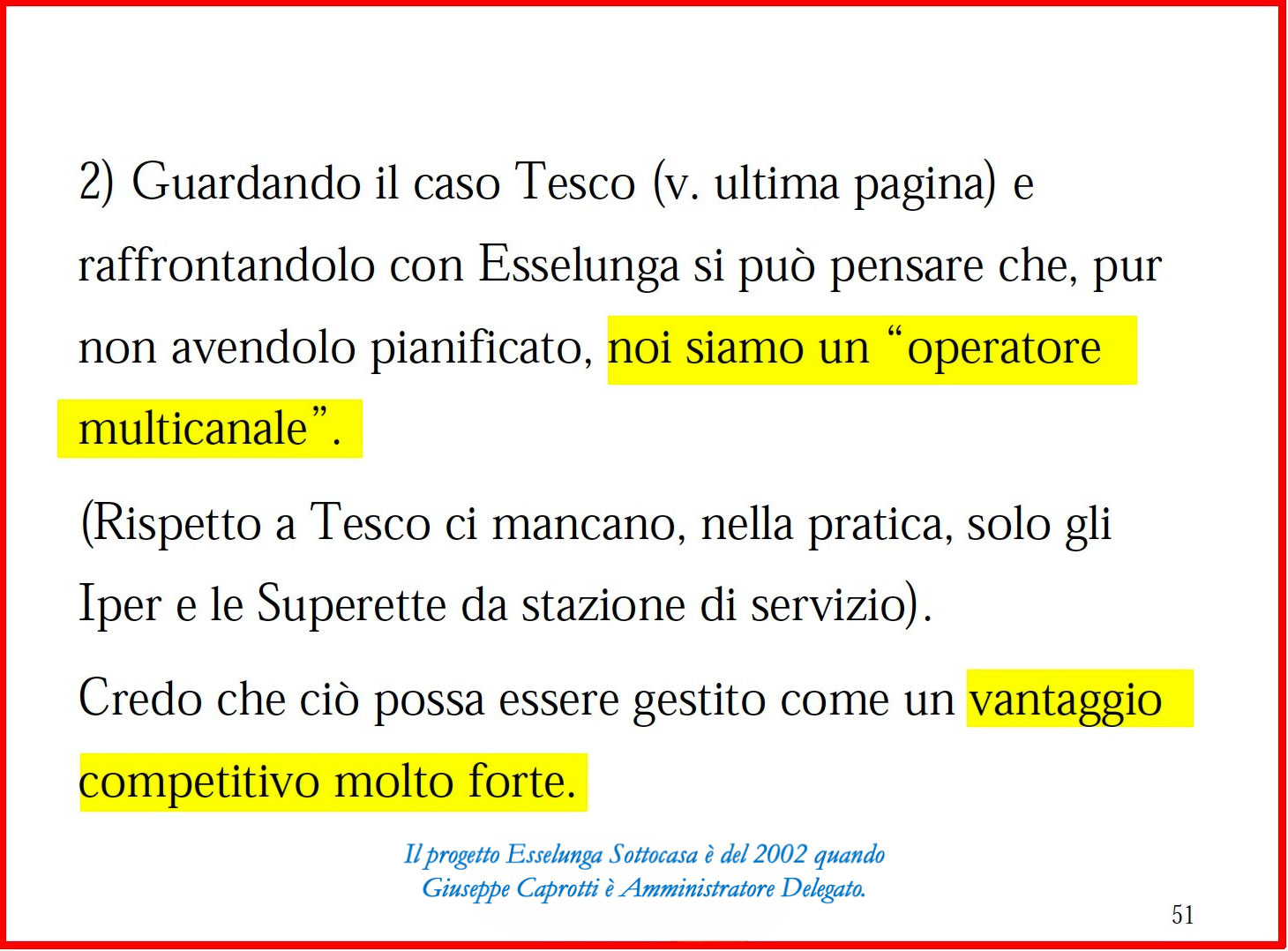

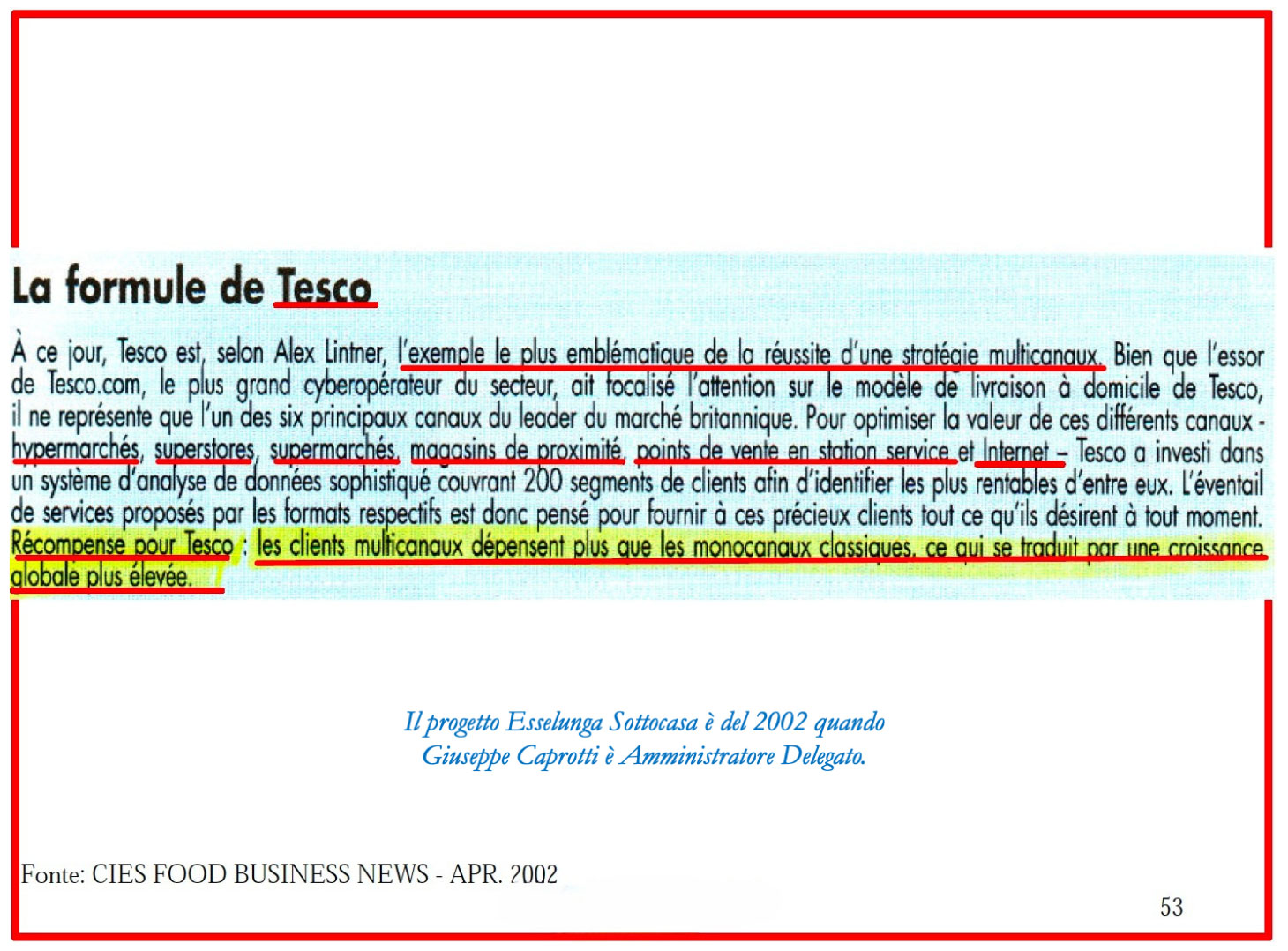

Interesting is the mention of Tesco which, at the time, was our model for Esselunga‘s e-commerce at home.

P.S.: I would like to add a reply given on LinkedIN to a comment on this article: Antonio Miele Excuse me, but I take the opportunity of this comment to clarify, I hope once and for all, what happened: my father made the superstores, I filled them. Then, about ten years later, I realised that the market was changing and I made a proposal – the Sottocasa – which he did not accept. If Esselunga is in difficulty today – so I read – it is also due to this refusal and to an erroneous industrial plan that focused all development on superstores. Personal opinion, not judgement, for goodness sake.

Demographic aspects of the project and profitability analysis

Technical note: there are two presentations and they have been aggregated. When reference is made in chart 51 to the last chart – about Tesco – this refers to No. 53.

Current margins of current Esselunga shops have been removed for confidentiality issues.